If you are planning to buy a home you may hear about the TRID or TILA-RESPA Integrated Disclosure. TRID is an effort put in place by the Consumer Financial Protection Bureau (CFPB) to protect home buyers from hidden fees and other abuses on the part of real estate agents, lenders and title companies.If you are planning to buy a home you may hear about the TRID or TILA-RESPA Integrated Disclosure. TRID is an effort put in place by the Consumer Financial Protection Bureau (CFPB) to protect home buyers from hidden fees and other abuses on the part of real estate agents, lenders and title companies.

If you are planning to buy a home you may hear about the TRID or TILA-RESPA Integrated Disclosure. TRID is an effort put in place by the Consumer Financial Protection Bureau (CFPB) to protect home buyers from hidden fees and other abuses on the part of real estate agents, lenders and title companies.If you are planning to buy a home you may hear about the TRID or TILA-RESPA Integrated Disclosure. TRID is an effort put in place by the Consumer Financial Protection Bureau (CFPB) to protect home buyers from hidden fees and other abuses on the part of real estate agents, lenders and title companies.

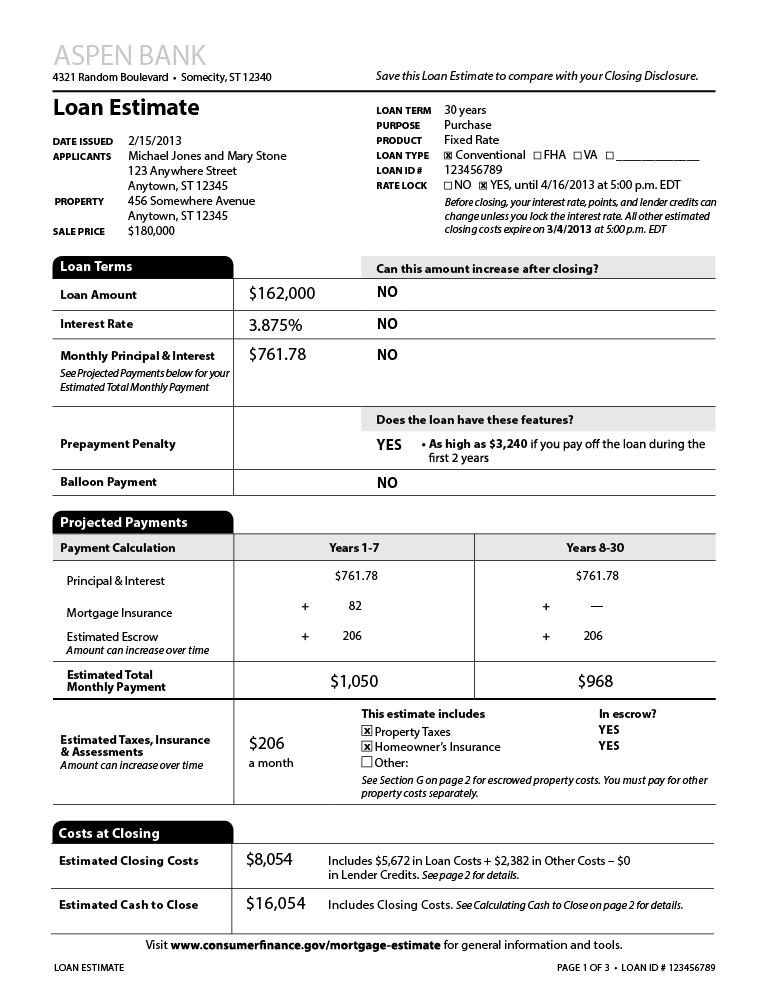

The CFPB condensed all the various fee disclosures and mortgage rate documents into two standardized forms. The two forms- the Loan Estimate and the Closing Disclosure- will play a major role in the loan process.

The Loan Estimate document (an example is attached in the link) is supposed to be received within 3 days after you apply for a loan. Something a potential buyer should keep in mind to avoid is shopping for the lowest mortgage interest rate, and not understanding how other costs factor into exactly what they will be paying. Home buyers should instead look at the entire package, and all the costs of each program.

The Closing Disclosure (an example is attached in the link) is similar to the Loan Estimate document, but it also includes information on the loan terms, adding a detailed list of what is being paid and by whom—buyer, seller and third parties. Note that the creditor must deliver the Closing Disclosure at least 3 days prior to the date of consummation (the day the consumer becomes contractually obligated on the loan) of the transaction.

Two other documents you should keep a close eye onare the Promissory Note, and the Security Instrument. The Promissory Note will list all the details of the loan, and will also say that your home is collateral. The Security Instrument, depending on what state you are located in, will require a signature on a mortgage or a deed of trust. Ultimately, the goal of this document is the pledge the home as security for the loan.

The good news, according to ClosingCorp, is that more than half of buyers say the TRID, also known as the “Know Before You Owe” forms are easier to understand than the forms that were used previously.

Make sure you completely trust your real estate agent and your lender- they are your biggest allies in this process. They will navigate and guide you, and explain everything that may be unclear.

For more information on TRID, please contact one of our loan specialists to get the down-low.

{kind=link}